U.S. International Transactions

Fourth Quarter and Year 2018

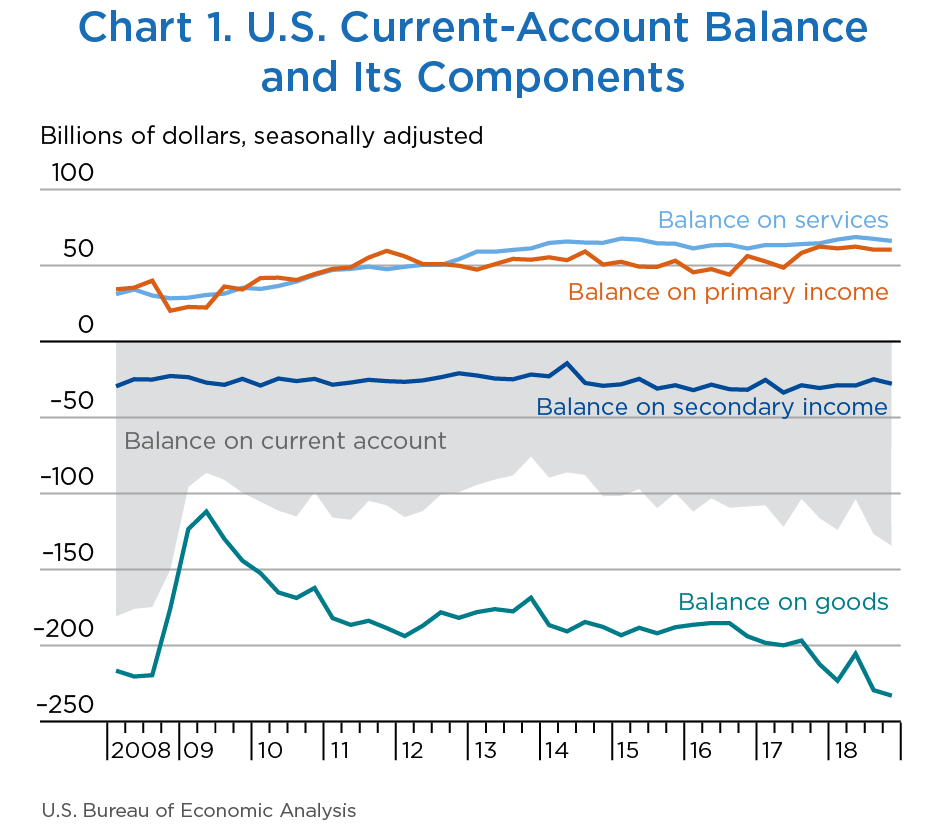

The U.S. current-account deficit—a net measure of transactions between the United States and the rest of the world in goods, services, primary income, and secondary income—increased to $134.4 billion (preliminary) in the fourth quarter of 2018 from $126.6 billion (revised) in the third quarter (chart 1 and table A). The deficit was 2.6 percent of current-dollar gross domestic product (GDP) in the fourth quarter, up from 2.5 percent in the third quarter.

The $7.8 billion increase in the current-account deficit mainly reflected increases in the deficits on goods and on secondary income and a decrease in the surplus on services.

[Click chart to expand]

Net U.S. borrowing measured by financial-account transactions was $168.3 billion in the fourth quarter, an increase from net borrowing of $36.8 billion in the third quarter.

The annual current-account deficit increased to $488.5 billion (preliminary) in 2018 from $449.1 billion in 2017. The deficit was 2.4 percent of current-dollar GDP in 2018, up from 2.3 percent in 2017.

Net U.S. borrowing measured by financial-account transactions was $519.6 billion in 2018, an increase from net borrowing of $331.9 billion in 2017.

| 2018 | Change 2018:III to 2018:IV | ||||

|---|---|---|---|---|---|

| Ir | IIr | IIIr | IVp | ||

| Current account | |||||

| Exports of goods and services and income receipts (credits) | 903,027 | 934,221 | 930,192 | 934,254 | 4,062 |

| Exports of goods and services | 615,222 | 633,033 | 627,086 | 625,415 | −1,671 |

| Goods | 409,210 | 427,198 | 419,830 | 416,094 | −3,736 |

| Services | 206,012 | 205,835 | 207,257 | 209,321 | 2,064 |

| Primary income receipts | 255,972 | 266,192 | 266,297 | 271,901 | 5,604 |

| Secondary income (current transfer) receipts | 31,833 | 34,996 | 36,809 | 36,938 | 129 |

| Imports of goods and services and income payments (debits) | 1,026,950 | 1,037,789 | 1,056,796 | 1,068,631 | 11,835 |

| Imports of goods and services | 771,478 | 769,908 | 789,097 | 792,379 | 3,282 |

| Goods | 632,478 | 632,723 | 649,303 | 649,147 | −156 |

| Services | 139,000 | 137,185 | 139,794 | 143,231 | 3,437 |

| Primary income payments | 194,783 | 203,860 | 205,958 | 211,465 | 5,507 |

| Secondary income (current transfer) payments | 60,689 | 64,021 | 61,740 | 64,787 | 3,047 |

| Capital account | |||||

| Capital transfer receipts and other credits | 0 | 0 | 562 | 8,856 | 8,294 |

| Capital transfer payments and other debits | 2 | 5 | 3 | n.a. | n.a. |

| Financial account | |||||

| Net U.S. acquisition of financial assets excluding financial derivatives (net increase in assets / financial outflow (+)) | 251,218 | −199,905 | 78,338 | 171,967 | 93,629 |

| Direct investment assets | −139,234 | −68,023 | 60,396 | 96,229 | 35,833 |

| Portfolio investment assets | 304,094 | −14,272 | 70,072 | −149,565 | −219,637 |

| Other investment assets | 86,365 | −120,679 | −51,953 | 223,199 | 275,152 |

| Reserve assets | −7 | 3,068 | −177 | 2,105 | 2,282 |

| Net U.S. incurrence of liabilities excluding financial derivatives (net increase in liabilities / financial inflow (+)) | 440,981 | −63,211 | 102,926 | 320,216 | 217,290 |

| Direct investment liabilities | 57,850 | 16,551 | 104,506 | 88,175 | −16,331 |

| Portfolio investment liabilities | 301,503 | 20,596 | 10,760 | −12,853 | −23,613 |

| Other investment liabilities | 81,628 | −100,358 | −12,340 | 244,895 | 257,235 |

| Financial derivatives other than reserves, net transactions | 29,024 | −16,969 | −12,255 | −20,061 | −7,806 |

| Statistical discrepancy | |||||

| Statistical discrepancy1 | −36,814 | −50,090 | 89,202 | −42,789 | −131,991 |

| Balances | |||||

| Balance on current account | −123,923 | −103,568 | −126,604 | −134,377 | −7,773 |

| Balance on goods and services | −156,256 | −136,875 | −162,011 | −166,964 | −4,953 |

| Balance on goods | −223,268 | −205,525 | −229,474 | −233,053 | −3,579 |

| Balance on services | 67,012 | 68,650 | 67,462 | 66,090 | −1,372 |

| Balance on primary income | 61,189 | 62,332 | 60,339 | 60,435 | 96 |

| Balance on secondary income | −28,856 | −29,026 | −24,931 | −27,849 | −2,918 |

| Balance on capital account | −2 | −5 | 559 | 8,856 | 8,297 |

| Net lending (+) or net borrowing (-) from current- and capital-account transactions2 | −123,925 | −103,573 | −126,045 | −125,521 | 524 |

| Net lending (+) or net borrowing (-) from financial-account transactions3 | −160,739 | −153,664 | −36,843 | −168,310 | −131,467 |

- p

- Preliminary

- r

- Revised

- n.a.

- Not available

- The statistical discrepancy is the difference between net acquisition of financial assets and net incurrence of liabilities in the financial account (including financial derivatives) less the difference between total credits and total debits recorded in the current and capital accounts.

- Sum of current- and capital-account balances.

- Sum of net U.S. acquisition of financial assets and net transactions in financial derivatives less net U.S. incurrence of liabilities.

Note. The statistics are presented in table 1.2 on BEA’s website.

Current-account highlights

- The deficit on goods increased $3.6 billion in the fourth quarter to $233.1 billion.

- The surplus on services decreased $1.4 billion to $66.1 billion.

- The surplus on primary income increased $0.1 billion to $60.4 billion.

- The deficit on secondary income increased $2.9 billion to $27.8 billion.

Capital-account highlights

Capital-transfer receipts were $8.9 billion in the fourth quarter. The transactions reflected receipts from foreign insurance companies for losses resulting from the wildfires in California. For information on transactions associated with natural disasters, see “What are the effects of hurricanes and other disasters on the international economic accounts?”

Financial-account highlights

- Net U.S. acquisition of financial assets excluding financial derivatives increased $93.6 billion to $172.0 billion (chart 2).

- Net U.S. incurrence of liabilities excluding financial derivatives increased $217.3 billion to $320.2 billion.

- Transactions in financial derivatives other than reserves reflected fourth-quarter net borrowing of $20.1 billion, a $7.8 billion increase in net borrowing from the third quarter.

[Click chart to expand]

Statistical discrepancy

The statistical discrepancy was –$42.8 billion in the fourth quarter following a statistical discrepancy of $89.2 billion in the third quarter.

Exports of goods and services and income receipts increased $4.1 billion, or 0.4 percent, in the fourth quarter to $934.3 billion (charts 3 and 4 and table B).

- Primary income receipts increased $5.6 billion, or 2.1 percent, to $271.9 billion, primarily reflecting increases in portfolio investment income and in other investment income. A decrease in direct investment income partly offset the increases. For more information on direct investment income, see “Effects of the 2017 Tax Cuts and Jobs Act on Components of the International Transactions Accounts.”

- Services exports increased $2.1 billion, or 1.0 percent, to $209.3 billion, mostly reflecting increases in other business services, primarily professional and management services; in travel (for all purposes including education), primarily personal travel; and in financial services.

- Goods exports decreased $3.7 billion, or 0.9 percent, to $416.1 billion, mainly reflecting a decrease in foods, feeds, and beverages, mostly soybeans.

[Click chart to expand]

[Click chart to expand]

| 2018 | Change 2018:III to 2018:IV | ||||

|---|---|---|---|---|---|

| Ir | IIr | IIIr | IVp | ||

| Exports of goods and services and income receipts | 903,027 | 934,221 | 930,192 | 934,254 | 4,062 |

| Exports of goods | 409,210 | 427,198 | 419,830 | 416,094 | −3,736 |

| General merchandise | 402,694 | 421,872 | 413,725 | 411,818 | −1,907 |

| Foods, feeds, and beverages | 31,369 | 38,552 | 34,254 | 29,077 | −5,177 |

| Industrial supplies and materials | 125,379 | 134,692 | 135,330 | 136,366 | 1,036 |

| Energy products | 46,929 | 54,162 | 55,619 | 58,072 | 2,453 |

| Of which: Petroleum and products | 40,071 | 47,041 | 48,935 | 50,442 | 1,507 |

| Nonenergy products | 78,450 | 80,530 | 79,711 | 78,294 | −1,417 |

| Capital goods except automotive | 138,221 | 141,658 | 140,294 | 142,099 | 1,805 |

| Automotive vehicles, parts, and engines | 42,177 | 40,304 | 38,776 | 37,340 | −1,436 |

| Consumer goods except food and automotive | 51,409 | 51,093 | 51,013 | 51,863 | 850 |

| Other general merchandise | 14,138 | 15,572 | 14,057 | 15,072 | 1,015 |

| Net exports of goods under merchanting | 66 | 77 | 70 | 64 | −6 |

| Nonmonetary gold | 6,450 | 5,249 | 6,034 | 4,212 | −1,822 |

| Exports of services1 | 206,012 | 205,835 | 207,257 | 209,321 | 2,064 |

| Maintenance and repair services n.i.e. | 7,289 | 7,471 | 7,684 | 7,598 | −86 |

| Transport | 22,951 | 23,455 | 22,885 | 23,013 | 128 |

| Travel (for all purposes including education) | 53,489 | 53,636 | 53,376 | 53,968 | 592 |

| Business | 9,883 | 9,737 | 9,705 | 9,713 | 8 |

| Personal | 43,606 | 43,899 | 43,671 | 44,255 | 584 |

| Insurance services | 4,555 | 4,557 | 5,017 | 5,035 | 18 |

| Financial services | 27,909 | 28,226 | 28,278 | 28,630 | 352 |

| Charges for the use of intellectual property n.i.e. | 33,577 | 32,400 | 32,209 | 32,265 | 56 |

| Telecommunications, computer, and information services | 10,911 | 10,628 | 11,163 | 11,257 | 94 |

| Other business services | 40,582 | 40,159 | 41,711 | 42,338 | 627 |

| Government goods and services n.i.e. | 4,748 | 5,304 | 4,933 | 5,218 | 285 |

| Primary income receipts | 255,972 | 266,192 | 266,297 | 271,901 | 5,604 |

| Investment income | 254,378 | 264,587 | 264,681 | 270,284 | 5,603 |

| Direct investment income | 134,983 | 140,099 | 138,869 | 137,864 | −1,005 |

| Income on equity | 128,014 | 132,805 | 131,717 | 130,750 | −967 |

| Dividends and withdrawals | 294,685 | 183,580 | 100,741 | 85,902 | −14,839 |

| Reinvested earnings | −166,671 | −50,775 | 30,975 | 44,848 | 13,873 |

| Interest | 6,969 | 7,293 | 7,152 | 7,114 | −38 |

| Portfolio investment income | 99,244 | 102,199 | 103,216 | 106,674 | 3,458 |

| Income on equity and investment fund shares | 65,937 | 67,344 | 67,921 | 71,075 | 3,154 |

| Interest on debt securities | 33,307 | 34,856 | 35,295 | 35,599 | 304 |

| Other investment income | 19,982 | 22,242 | 22,366 | 25,559 | 3,193 |

| Reserve asset income | 169 | 47 | 230 | 187 | −43 |

| Compensation of employees | 1,594 | 1,605 | 1,615 | 1,616 | 1 |

| Secondary income (current transfer) receipts2 | 31,833 | 34,996 | 36,809 | 36,938 | 129 |

- p

- Preliminary

- r

- Revised

- n.i.e.

- Not included elsewhere

- See also Shari A. Allen, Alexis N. Grimm, and Christopher P. Steiner, “U.S. International Services: Trade in Services in 2017 and Services Supplied Through Affiliates in 2016,” Survey of Current Business 98 (October 2018).

- Secondary income receipts include U.S. government and private transfers, such as fines and penalties, withholding taxes, insurance-related transfers, and other current transfers.

Imports of goods and services and income payments increased $11.8 billion, or 1.1 percent, in the fourth quarter to $1.1 trillion (charts 3 and 5 and table C).

- Primary income payments increased $5.5 billion, or 2.7 percent, to $211.5 billion, mainly reflecting increases in other investment income and in portfolio investment income.

- Services imports increased $3.4 billion, or 2.5 percent, to $143.2 billion, mostly reflecting increases in travel (for all purposes including education), primarily personal travel, and in transport, primarily sea freight transport and air passenger transport.

- Secondary income payments increased $3.0 billion, or 4.9 percent, to $64.8 billion, mostly reflecting an increase in U.S. government grants.

[Click chart to expand]

| 2018 | Change 2018:III to 2018:IV | ||||

|---|---|---|---|---|---|

| Ir | IIr | IIIr | IVp | ||

| Imports of goods and services and income payments | 1,026,950 | 1,037,789 | 1,056,796 | 1,068,631 | 11,835 |

| Imports of goods | 632,478 | 632,723 | 649,303 | 649,147 | −156 |

| General merchandise | 629,670 | 630,044 | 646,832 | 646,528 | −304 |

| Foods, feeds, and beverages | 37,001 | 37,077 | 37,083 | 37,270 | 187 |

| Industrial supplies and materials | 142,402 | 146,515 | 150,870 | 143,638 | −7,232 |

| Energy products | 62,199 | 64,728 | 68,468 | 60,056 | −8,412 |

| Of which: Petroleum and products | 58,747 | 61,324 | 64,979 | 55,747 | −9,232 |

| Nonenergy products | 80,203 | 81,787 | 82,402 | 83,582 | 1,180 |

| Capital goods except automotive | 170,623 | 174,194 | 176,726 | 175,039 | −1,687 |

| Automotive vehicles, parts, and engines | 92,914 | 90,179 | 93,802 | 96,302 | 2,500 |

| Consumer goods except food and automotive | 164,026 | 157,432 | 162,120 | 166,639 | 4,519 |

| Other general merchandise | 22,703 | 24,648 | 26,230 | 27,639 | 1,409 |

| Nonmonetary gold | 2,809 | 2,678 | 2,472 | 2,620 | 148 |

| Imports of services1 | 139,000 | 137,185 | 139,794 | 143,231 | 3,437 |

| Maintenance and repair services n.i.e. | 2,093 | 2,062 | 2,275 | 2,291 | 16 |

| Transport | 26,189 | 26,692 | 27,067 | 28,357 | 1,290 |

| Travel (for all purposes including education) | 35,435 | 35,502 | 35,650 | 37,570 | 1,920 |

| Business | 3,981 | 4,157 | 4,130 | 4,160 | 30 |

| Personal | 31,453 | 31,345 | 31,520 | 33,410 | 1,890 |

| Insurance services | 9,754 | 9,554 | 9,546 | 9,375 | −171 |

| Financial services | 7,534 | 7,719 | 7,715 | 7,822 | 107 |

| Charges for the use of intellectual property n.i.e. | 13,921 | 13,048 | 13,448 | 13,335 | −113 |

| Telecommunications, computer, and information services | 10,172 | 9,828 | 10,210 | 10,206 | −4 |

| Other business services | 28,251 | 27,048 | 28,074 | 28,492 | 418 |

| Government goods and services n.i.e. | 5,653 | 5,731 | 5,809 | 5,785 | −24 |

| Primary income payments | 194,783 | 203,860 | 205,958 | 211,465 | 5,507 |

| Investment income | 189,797 | 198,793 | 200,875 | 206,355 | 5,480 |

| Direct investment income | 57,381 | 61,023 | 60,149 | 59,336 | −813 |

| Portfolio investment income | 114,968 | 116,895 | 116,746 | 118,815 | 2,069 |

| Income on equity and investment fund shares | 38,844 | 40,216 | 39,338 | 41,039 | 1,701 |

| Interest on debt securities | 76,124 | 76,678 | 77,408 | 77,776 | 368 |

| Other investment income | 17,448 | 20,875 | 23,979 | 28,204 | 4,225 |

| Compensation of employees | 4,986 | 5,067 | 5,084 | 5,110 | 26 |

| Secondary income (current transfer) payments2 | 60,689 | 64,021 | 61,740 | 64,787 | 3,047 |

| Supplemental detail on insurance transactions: | |||||

| Premiums paid | 23,986 | 24,557 | 25,140 | 25,092 | −48 |

| Losses recovered | 18,689 | 18,935 | 19,545 | 27,839 | 8,294 |

- p

- Preliminary

- r

- Revised

- n.i.e.

- Not included elsewhere

- See also Shari A. Allen, Alexis N. Grimm, and Christopher P. Steiner, “U.S. International Services: Trade in Services in 2017 and Services Supplied Through Affiliates in 2016,” Survey of Current Business 98 (October 2018).

- Secondary income payments include U.S. government and private transfers, such as U.S. government grants and pensions, fines and penalties, withholding taxes, personal transfers (remittances), insurance-related transfers, and other current transfers.

Acquisition of financial assets

- Net U.S. acquisition of other investment assets was $223.2 billion following net U.S. liquidation of $52.0 billion in the third quarter (chart 6 and table D). This change mostly reflected net U.S acquisition of currency and deposits and net U.S. provision of loans to foreign residents following net withdrawal of U.S. deposits from foreign banks and net foreign repayment of loans in the third quarter.

- Net U.S. sales of portfolio investment assets were $149.6 billion following net U.S. purchases of $70.1 billion in the third quarter. This change reflected net U.S. sales of both equity and debt instruments following net U.S. purchases in the third quarter.

- Net U.S. acquisition of direct investment assets increased $35.8 billion to $96.2 billion. For more information on recent transactions in direct investment assets, see “Effects of the 2017 Tax Cuts and Jobs Act on Components of the International Transactions Accounts.”

Incurrence of liabilities

Net U.S. incurrence of other investment liabilities was $244.9 billion following net U.S. repayment of $12.3 billion in the third quarter. This change primarily reflected net foreign provision of loans and net U.S. incurrence of currency and deposits following net U.S. repayment of loans and net foreign withdrawal of currency and deposits in the third quarter.

[Click chart to expand]

| 2018 | Change 2018:III to 2018:IV | ||||

|---|---|---|---|---|---|

| Ir | IIr | IIIr | IVp | ||

| Net U.S. acquisition of financial assets excluding financial derivatives (net increase in assets / financial outflow (+)) | 251,218 | −199,905 | 78,338 | 171,967 | 93,629 |

| Direct investment assets | −139,234 | −68,023 | 60,396 | 96,229 | 35,833 |

| Equity | −167,640 | −52,771 | 64,334 | 97,536 | 33,202 |

| Equity other than reinvestment of earnings | −969 | −1,996 | 33,359 | 52,688 | 19,329 |

| Reinvestment of earnings | −166,671 | −50,775 | 30,975 | 44,848 | 13,873 |

| Debt instruments | 28,406 | −15,252 | −3,939 | −1,307 | 2,632 |

| Portfolio investment assets | 304,094 | −14,272 | 70,072 | −149,565 | −219,637 |

| Equity and investment fund shares | 200,871 | −70,830 | 32,245 | −65,105 | −97,350 |

| Debt securities | 103,223 | 56,559 | 37,828 | −84,460 | −122,288 |

| Short-term securities | 27,771 | 2,469 | 21,546 | −34,190 | −55,736 |

| Long-term corporate securities | 53,741 | 37,717 | 11,435 | −36,588 | −48,023 |

| Other long-term securities | 21,711 | 16,373 | 4,847 | −13,682 | −18,529 |

| Other investment assets | 86,365 | −120,679 | −51,953 | 223,199 | 275,152 |

| Currency and deposits | 53,816 | −22,388 | −23,109 | 143,516 | 166,625 |

| Loans | 33,356 | −99,576 | −27,225 | 77,718 | 104,943 |

| Trade credit and advances | −807 | 1,285 | −1,618 | 1,964 | 3,582 |

| Reserve assets | −7 | 3,068 | −177 | 2,105 | 2,282 |

| Monetary gold | 0 | 0 | 0 | 0 | 0 |

| Special drawing rights | 33 | 33 | 43 | 47 | 4 |

| Reserve position in the International Monetary Fund | −73 | 3,136 | −288 | 2,049 | 2,337 |

| Other reserve assets | 34 | −101 | 68 | 9 | −59 |

| Net U.S. incurrence of liabilities excluding financial derivatives (net increase in liabilities / financial inflow (+)) | 440,981 | −63,211 | 102,926 | 320,216 | 217,290 |

| Direct investment liabilities | 57,850 | 16,551 | 104,506 | 88,175 | −16,331 |

| Equity | 72,562 | 45,505 | 114,541 | 99,600 | −14,941 |

| Equity other than reinvestment of earnings | 37,499 | 10,591 | 77,886 | 68,982 | −8,904 |

| Reinvestment of earnings | 35,063 | 34,913 | 36,655 | 30,618 | −6,037 |

| Debt instruments | −14,712 | −28,954 | −10,035 | −11,425 | −1,390 |

| Portfolio investment liabilities | 301,503 | 20,596 | 10,760 | −12,853 | −23,613 |

| Equity and investment fund shares | 154,313 | 291 | −95,528 | 88,160 | 183,688 |

| Debt securities | 147,190 | 20,305 | 106,287 | −101,013 | −207,300 |

| Short term | 31,355 | 37,436 | −53,098 | 13,079 | 66,177 |

| Treasury bills and certificates | 13,560 | 33,709 | −35,170 | 30,182 | 65,352 |

| Federally sponsored agency securities | 2,214 | −680 | −6,121 | −2,081 | 4,040 |

| Other short-term securities | 15,581 | 4,407 | −11,807 | −15,022 | −3,215 |

| Long term | 115,835 | −17,131 | 159,386 | −114,093 | −273,479 |

| Treasury bonds and notes | 73,078 | −12,004 | 99,265 | −87,053 | −186,318 |

| Federally sponsored agency securities | 37,775 | 6,518 | 19,575 | 16,574 | −3,001 |

| Corporate bonds and notes | 4,731 | −13,257 | 40,733 | −42,175 | −82,908 |

| Other | 251 | 1,612 | −187 | −1,439 | −1,252 |

| Other investment liabilities | 81,628 | −100,358 | −12,340 | 244,895 | 257,235 |

| Currency | 16,970 | 19,391 | 19,606 | 9,364 | −10,242 |

| Deposits | −27,004 | −77,318 | −26,640 | 95,218 | 121,858 |

| Loans | 82,566 | −47,064 | −7,584 | 141,815 | 149,399 |

| Trade credit and advances | 9,096 | 4,634 | 2,278 | −1,502 | −3,780 |

| Special drawing rights allocations | 0 | 0 | 0 | 0 | 0 |

In the international transactions accounts, income on equity, or earnings, of foreign affiliates of U.S. multinational enterprises consists of a portion that is repatriated to the parent company in the United States in the form of dividends and a portion that is reinvested in foreign affiliates. At times, repatriation of dividends exceeds current-period earnings, resulting in negative values being recorded for reinvested earnings. In 2018, dividends exceeded earnings, reflecting the repatriation of accumulated prior earnings of foreign affiliates of U.S. multinational enterprises by their parent companies in the United States in response to the 2017 Tax Cuts and Jobs Act (TCJA), which generally eliminated taxes on repatriated earnings. Dividends were $664.9 billion while reinvested earnings were –$141.6 billion (chart 7 and tables B and E). The reinvested earnings are also reflected in the net acquisition of direct investment assets in the financial account (table D).

For more information, see “How does the 2017 Tax Cuts and Jobs Act affect BEA's business income statistics?” and “How are the International Transactions Accounts affected by an increase in direct investment dividend receipts?”

[Click chart to expand]

| 2017 | 2018 | Annual | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | Ir | IIr | IIIr | IVp | 2017 | 2018p | |

| Direct investment earnings | 114.1 | 114.4 | 120.3 | 128.9 | 128.0 | 132.8 | 131.7 | 130.8 | 477.7 | 523.3 |

| Dividends | 38.2 | 34.9 | 55.1 | 26.9 | 294.7 | 183.6 | 100.7 | 85.9 | 155.1 | 664.9 |

| Reinvested earnings | 75.9 | 79.5 | 65.2 | 102.0 | −166.7 | −50.8 | 31.0 | 44.8 | 322.6 | −141.6 |

- p

- Preliminary

- r

- Revised

In addition to the repatriation of accumulated earnings, some companies made other changes to their business practices in reaction to the TCJA. For example, some insurance companies changed how they operate in response to the base erosion and anti-abuse tax (BEAT) provision of the TCJA. BEAT is a tax on certain payments from a U.S. company to a related foreign party, which can include premium payments for reinsurance. In response to the new tax, many U.S. insurance companies terminated these intracompany reinsurance contracts. As a result, premiums paid by U.S. insurers to foreign insurers in 2018 were $98.8 billion, down from $129.9 billion in 2017 (table C). Similarly, insurance services imports in 2018 were $38.2 billion, down from $50.7 billion in 2017.

For more information on the estimation methods used to compile insurance services, see the insurance section in “U.S. International Economic Accounts: Concepts and Methods.”

The U.S. international transactions statistics for the third quarter of 2018 have been updated to incorporate newly available and revised source data (table F). In addition, the statistics for the first three quarters of 2018 have been updated to align the seasonally adjusted statistics with annual totals.

| Preliminary Estimates | Revised Estimates | |

|---|---|---|

| Balance on current account | −124,817 | −126,604 |

| Balance on goods | −227,012 | −229,474 |

| Balance on services | 68,356 | 67,462 |

| Balance on primary income | 59,425 | 60,339 |

| Balance on secondary income (current transfers) | −25,586 | −24,931 |

| Net lending or borrowing from financial-account transactions | −31,289 | −36,843 |

| Net U.S. acquisition of financial assets | 132,689 | 78,338 |

| Net U.S. incurrence of liabilities | 151,723 | 102,926 |

| Financial derivatives other than reserves, net transactions | −12,255 | −12,255 |

Current-account highlights

In 2018, the current-account deficit increased $39.3 billion, or 8.8 percent, reflecting an increase in the deficit on goods that was partly offset by increases in the surpluses on primary income and on services and a decrease in the deficit on secondary income (chart 8 and table G).

Exports of goods and services and income receipts

Exports of goods and services and income receipts increased $268.5 billion, or 7.8 percent, in 2018 to $3.7 trillion (chart 9).

- Primary income receipts increased $132.2 billion, or 14.2 percent, to $1.1 trillion, led by increases in portfolio investment income and in direct investment income.

- Goods exports increased $118.9 billion, or 7.7 percent, to $1.7 trillion, led by an increase in industrial supplies and materials, primarily petroleum and products.

- Services exports increased $30.7 billion, or 3.9 percent, to $0.8 trillion, led by an increase in other business services.

[Click chart to expand]

[Click chart to expand]

Imports of goods and services and income payments

Imports of goods and services and income payments increased $307.8 billion, or 7.9 percent, to $4.2 trillion (chart 10).

- Goods imports increased $202.8 billion, or 8.6 percent, to $2.6 trillion, led by increases in industrial supplies and materials, in capital goods, and in consumer goods.

- Primary income payments increased $109.7 billion, or 15.5 percent, to $0.8 trillion, led by an increase in other investment income.

[Click chart to expand]

| 2015 | 2016 | 2017 | 2018p | Change 2017 to 2018 | |

|---|---|---|---|---|---|

| Current account | |||||

| Exports of goods and services and income receipts (credits) | 3,207,288 | 3,183,783 | 3,433,239 | 3,701,694 | 268,455 |

| Exports of goods | 1,511,381 | 1,456,957 | 1,553,383 | 1,672,331 | 118,948 |

| Foods, feeds, and beverages | 127,721 | 130,519 | 132,744 | 133,253 | 509 |

| Industrial supplies and materials | 418,141 | 387,350 | 456,188 | 531,768 | 75,580 |

| Capital goods except automotive | 539,805 | 519,890 | 533,574 | 562,273 | 28,699 |

| Automotive vehicles, parts, and engines | 151,894 | 150,311 | 157,641 | 158,597 | 956 |

| Consumer goods except food and automotive | 197,318 | 193,254 | 197,134 | 205,378 | 8,244 |

| Other general merchandise | 54,917 | 54,791 | 54,358 | 58,840 | 4,482 |

| Net exports of goods under merchanting | 261 | 300 | 200 | 277 | 77 |

| Nonmonetary gold | 21,325 | 20,542 | 21,544 | 21,945 | 401 |

| Exports of services | 755,310 | 758,888 | 797,690 | 828,425 | 30,735 |

| Maintenance and repair services n.i.e. | 23,384 | 25,004 | 26,430 | 30,041 | 3,611 |

| Transport | 87,725 | 84,679 | 88,598 | 92,304 | 3,706 |

| Travel (for all purposes including education) | 206,936 | 206,902 | 210,747 | 214,469 | 3,722 |

| Insurance services | 16,248 | 17,067 | 18,047 | 19,164 | 1,117 |

| Financial services | 102,435 | 99,384 | 109,642 | 113,043 | 3,401 |

| Charges for the use of intellectual property n.i.e. | 124,769 | 124,734 | 128,364 | 130,451 | 2,087 |

| Telecommunications, computer, and information services | 36,578 | 38,548 | 42,219 | 43,959 | 1,740 |

| Other business services | 137,148 | 143,768 | 154,313 | 164,790 | 10,477 |

| Government goods and services n.i.e. | 20,087 | 18,801 | 19,329 | 20,202 | 873 |

| Primary income receipts | 810,073 | 830,174 | 928,118 | 1,060,362 | 132,244 |

| Direct investment income | 459,901 | 456,426 | 504,404 | 551,815 | 47,411 |

| Portfolio investment income | 312,028 | 326,325 | 354,406 | 411,334 | 56,928 |

| Other investment income | 31,346 | 40,850 | 62,620 | 90,150 | 27,530 |

| Reserve asset income | 219 | 108 | 385 | 632 | 247 |

| Compensation of employees | 6,578 | 6,466 | 6,302 | 6,431 | 129 |

| Secondary income (current transfer) receipts | 130,525 | 137,764 | 154,049 | 140,576 | −13,473 |

| Imports of goods and services and income payments (debits) | 3,615,053 | 3,616,656 | 3,882,380 | 4,190,166 | 307,786 |

| Imports of goods | 2,273,249 | 2,208,008 | 2,360,878 | 2,563,651 | 202,773 |

| Foods, feeds, and beverages | 128,762 | 131,024 | 138,810 | 148,431 | 9,621 |

| Industrial supplies and materials | 492,483 | 441,848 | 511,561 | 583,426 | 71,865 |

| Capital goods except automotive | 607,160 | 593,854 | 643,620 | 696,582 | 52,962 |

| Automotive vehicles, parts, and engines | 350,049 | 351,058 | 359,849 | 373,197 | 13,348 |

| Consumer goods except food and automotive | 596,417 | 585,177 | 603,922 | 650,217 | 46,295 |

| Other general merchandise | 85,789 | 86,887 | 90,913 | 101,220 | 10,307 |

| Nonmonetary gold | 12,590 | 18,160 | 12,203 | 10,578 | −1,625 |

| Imports of services | 491,966 | 509,838 | 542,471 | 559,211 | 16,740 |

| Maintenance and repair services n.i.e. | 9,013 | 8,731 | 8,337 | 8,721 | 384 |

| Transport | 97,006 | 96,939 | 101,744 | 108,305 | 6,561 |

| Travel (for all purposes including education) | 114,548 | 123,569 | 135,024 | 144,156 | 9,132 |

| Insurance services | 47,420 | 49,900 | 50,665 | 38,228 | −12,437 |

| Financial services | 25,769 | 25,752 | 28,931 | 30,790 | 1,859 |

| Charges for the use of intellectual property n.i.e. | 40,608 | 46,577 | 51,284 | 53,751 | 2,467 |

| Telecommunications, computer, and information services | 36,704 | 37,391 | 40,054 | 40,417 | 363 |

| Other business services | 99,368 | 99,476 | 104,385 | 111,865 | 7,480 |

| Government goods and services n.i.e. | 21,531 | 21,503 | 22,047 | 22,978 | 931 |

| Primary income payments | 606,464 | 637,151 | 706,386 | 816,066 | 109,680 |

| Direct investment income | 175,256 | 183,812 | 205,976 | 237,890 | 31,914 |

| Portfolio investment income | 398,584 | 407,603 | 432,510 | 467,424 | 34,914 |

| Other investment income | 14,968 | 26,599 | 48,213 | 90,506 | 42,293 |

| Compensation of employees | 17,656 | 19,139 | 19,687 | 20,246 | 559 |

| Secondary income (current transfer) payments | 243,372 | 261,659 | 272,645 | 251,237 | −21,408 |

| Balances | |||||

| Balance on current account | −407,764 | −432,873 | −449,142 | −488,472 | −39,330 |

| Balance on goods | −761,868 | −751,051 | −807,495 | −891,320 | −83,825 |

| Balance on services | 263,343 | 249,050 | 255,219 | 269,214 | 13,995 |

| Balance on primary income | 203,608 | 193,023 | 221,731 | 244,295 | 22,564 |

| Balance on secondary income | −112,848 | −123,895 | −118,597 | −110,661 | 7,936 |

- p

- Preliminary

- n.i.e.

- Not included elsewhere

Note. The statistics are presented in table 1.2 on BEA’s website.

Capital account

Capital transfer receipts were $9.4 billion in 2018 (table H). The transactions reflected receipts from foreign insurance companies for losses resulting from Hurricane Florence and the wildfires in California. For more information, see “What are the effects of hurricanes and other disasters on the international economic accounts?”

Acquisition of financial assets

Net U.S. acquisition of financial assets excluding financial derivatives decreased $881.1 billion to $301.6 billion.

- Net U.S. withdrawal of direct investment assets was $50.6 billion following net U.S. acquisition of $379.2 billion in 2017. The net withdrawal of direct investment assets reflected U.S. parent repatriation of previously reinvested earnings in response to the TCJA. For more information, see “Effects of the 2017 Tax Cuts and Jobs Act on Components of the International Transactions Accounts.”

- Net U.S. purchases of portfolio investment assets decreased $376.4 billion to $210.3 billion, mostly reflecting a decrease in net U.S. purchases of foreign debt securities.

- Net U.S. acquisition of other investment assets decreased $81.6 billion to $136.9 billion. This change mostly reflected net foreign repayment of loans following net U.S. provision in 2017.

Incurrence of liabilities

Net U.S. incurrence of liabilities excluding financial derivatives decreased $736.8 billion to $800.9 billion.

- Net foreign purchases of portfolio investment liabilities decreased $479.2 billion to $320.0 billion, mostly reflecting a decrease in net foreign purchases of U.S. bonds.

- Net U.S. incurrence of other investment liabilities decreased $169.8 billion to $213.8 billion, mainly reflecting a decrease in net U.S. incurrence of currency and deposits.

- Net U.S. incurrence of direct investment liabilities decreased $87.7 billion to $267.1 billion, mainly reflecting net U.S. repayment of debt liabilities following net U.S. incurrence in 2017.

Financial derivatives

Transactions in financial derivatives other than reserves reflected net borrowing of $20.3 billion in 2018 following net lending of $23.1 billion in 2017.

Statistical discrepancy

The statistical discrepancy was –$40.5 billion in 2018 following a statistical discrepancy of $92.5 billion in 2017.

| 2015 | 2016 | 2017 | 2018p | Change 2017 to 2018 | |

|---|---|---|---|---|---|

| Capital account | |||||

| Capital transfer receipts and other credits | 0 | 0 | 24,788 | 9,418 | −15,370 |

| Capital transfer payments and other debits | 42 | 59 | 42 | 10 | −32 |

| Financial account | |||||

| Net U.S. acquisition of financial assets excluding financial derivatives (net increase in assets / financial outflow (+)) | 202,208 | 348,625 | 1,182,749 | 301,618 | −881,131 |

| Direct investment assets | 307,058 | 312,975 | 379,222 | −50,633 | −429,855 |

| Equity | 297,440 | 336,657 | 352,504 | −58,540 | −411,044 |

| Equity other than reinvestment of earnings | 7,626 | 43,747 | 29,878 | 83,082 | 53,204 |

| Reinvestment of earnings | 289,814 | 292,910 | 322,626 | −141,622 | −464,248 |

| Debt instruments | 9,618 | −23,683 | 26,718 | 7,907 | −18,811 |

| Portfolio investment assets | 160,410 | 36,283 | 586,695 | 210,330 | −376,365 |

| Equity and investment fund shares | 196,922 | 21,743 | 166,827 | 97,180 | −69,647 |

| Debt securities | −36,511 | 14,541 | 419,868 | 113,150 | −306,718 |

| Short term | 43,045 | −27,409 | 193,855 | 17,596 | −176,259 |

| Long term | −79,556 | 41,950 | 226,013 | 95,554 | −130,459 |

| Other investment assets | −258,968 | −2,723 | 218,522 | 136,932 | −81,590 |

| Currency and deposits | −191,472 | −91,317 | 171,952 | 151,834 | −20,118 |

| Loans | −65,793 | 87,690 | 40,862 | −15,727 | −56,589 |

| Trade credit and advances | −1,702 | 903 | 5,708 | 825 | −4,883 |

| Reserve assets | −6,292 | 2,090 | −1,690 | 4,989 | 6,679 |

| Monetary gold | 0 | 0 | 0 | 0 | 0 |

| Special drawing rights | 9 | 684 | 78 | 156 | 78 |

| Reserve position in the International Monetary Fund | −6,485 | 1,348 | −1,812 | 4,824 | 6,636 |

| Other reserve assets | 185 | 58 | 44 | 10 | −34 |

| Net U.S. incurrence of liabilities excluding financial derivatives (net increase in liabilities / financial inflow (+)) | 501,121 | 741,529 | 1,537,683 | 800,913 | −736,770 |

| Direct investment liabilities | 509,087 | 494,455 | 354,829 | 267,081 | −87,748 |

| Equity | 423,974 | 387,599 | 308,406 | 332,207 | 23,801 |

| Equity other than reinvestment of earnings | 340,867 | 295,955 | 200,547 | 194,958 | −5,589 |

| Reinvestment of earnings | 83,107 | 91,644 | 107,859 | 137,250 | 29,391 |

| Debt instruments | 85,114 | 106,856 | 46,423 | −65,126 | −111,549 |

| Portfolio investment liabilities | 213,910 | 231,349 | 799,182 | 320,006 | −479,176 |

| Equity and investment fund shares | −187,306 | −139,700 | 155,680 | 147,236 | −8,444 |

| Debt securities | 401,216 | 371,049 | 643,503 | 172,769 | −470,734 |

| Short term | 45,833 | −12,092 | 15,851 | 28,772 | 12,921 |

| Long term | 355,383 | 383,141 | 627,652 | 143,997 | −483,655 |

| Other investment liabilities | −221,876 | 15,725 | 383,671 | 213,826 | −169,845 |

| Currency and deposits | 35,103 | 17,199 | 217,427 | 29,587 | −187,840 |

| Loans | −264,970 | −7,574 | 150,834 | 169,734 | 18,900 |

| Trade credit and advances | 7,991 | 6,101 | 15,410 | 14,505 | −905 |

| Special drawing rights allocations | 0 | 0 | 0 | 0 | 0 |

| Financial derivatives other than reserves, net transactions | −27,035 | 7,827 | 23,074 | −20,261 | −43,335 |

| Statistical discrepancy | |||||

| Statistical discrepancy1 | 81,859 | 47,855 | 92,536 | −40,492 | −133,028 |

| Balances | |||||

| Balance on capital account | −42 | −59 | 24,746 | 9,409 | −15,337 |

| Net lending (+) or net borrowing (-) from current- and capital-account transactions2 | −407,807 | −432,932 | −424,395 | −479,064 | −54,669 |

| Net lending (+) or net borrowing (-) from financial-account transactions3 | −325,948 | −385,078 | −331,860 | −519,556 | −187,696 |

- p

- Preliminary

- The statistical discrepancy is the difference between net acquisition of assets and net incurrence of liabilities in the financial account (including financial derivatives) less the difference between total credits and total debits recorded in the current and capital accounts.

- Sum of current-account balance (table G) and capital-account balance.

- Sum of net U.S. acquisition of financial assets and net transactions in financial derivatives less net U.S. incurrence of liabilities.